How Private Trust Companies in the Cook Islands Can Help Safeguard Your Wealth: A Comprehensive Guide

Private trust companies (“PTCs”) are established with the sole purpose of acting as a corporate trustee to one or more family, or otherwise related, trusts and are becoming increasingly popular with settlors when deciding who to appoint as trustee of their trusts. This is inevitably due to a settlor’s understandable reluctance to hand over ownership and control of their assets to people they don’t know and who might be based in a country that they never visited.

The Cook Islands has seen a growing number of Cook Islands international companies (“ICs”) being registered for the purpose of acting as a PTC, as ICs provide a convenient, flexible and easy-to-administer PTC option.

Advantages of PTCs

Using a PTC can offer a settlor numerous benefits and advantages when compared to using a professional or other completely independent trustee. Those benefits and advantages include:

Peace of mind: the settlor may find greater comfort having the trust assets owned and administered by a PTC that they have created and can control;

Control: a PTC allows the settlor, or those they nominate, to retain a high degree of control over the administration of trust assets, including investment and distribution decisions. This can be achieved by the settlor and his/her family members and advisors becoming directors of the PTC;

Confidentiality: a PTC enables better control over information confidential to the settlor and their family;

Diversification: a PTC will provide the settlor a greater opportunity to invest in and hold assets of their choice. A trustee has a duty to preserve and diversify trust assets in the best interests of all beneficiaries. A professional corporate trustee may therefore be averse to holding high-risk assets or a high percentage of the same assets to avoid breaching its duty;

Expense: a PTC allows the settlor to avoid professional trustee fees and other professional costs, which for larger trust funds are often charged on an ad valorem basis.

Important Questions when establishing a PTC

When establishing a PTC to act as trustee, a settlor, and their advisors, need to address several important questions, including:

- In which jurisdiction will the PTC be incorporated?

- Does that jurisdiction have competent and trustworthy service providers?

- How is the PTC established?

- Who will be appointed to the board of directors?

- What will be the ownership structure of the PTC?

- Will the PTC be as effective in protecting trust assets as a professional trustee?

This is how the Cook Islands answers those questions, proving it offers a PTC solution to meet the needs of every settlor.

Jurisdiction of Choice

Ideally, the jurisdiction of choice for the PTC should be reputable, politically stable and compliant with international best practice. Service providers must be regulated with a level of experience, expertise and integrity that provides comfort to clients and their advisors. They must be accessible and responsive. The laws must be robust, tested and designed to meet the needs of today’s society.

The Cook Islands is a sovereign nation and can therefore make its own laws. It has a Westminster-style parliamentary democracy and a strong history of respect for the rule of law, having always been politically stable with no threat of military or social unrest. Over the past 40 years, the Cook Islands has become a world leader in the preservation and protection of wealth by developing a legal framework focused on protecting wealth and the rights of its owners. The Cook Islands trust, foundation and company laws each contain provisions providing certainty to settlors, founders and beneficial owners, as well as third parties, as to the rights of those who might claim against assets by reference to specific dates and events.

The Cook Islands is located north-east of New Zealand and south-west of Hawaii in the middle of the South Pacific, providing a time zone convenient for doing same-day business with Asia and the USA.

The Cook Islands is meeting international standards on the exchange of financial information, harmful tax practices and combating financial crime. It is not on any of the blacklists published by international organisations, such as the OECD, FATF and EU, proving itself to be a good international citizen.

Local Service Providers

The Cook Islands has been providing wealth management, fiduciary and administration services internationally for over 40 years. It has several licensed trustee companies (“LTCs”) that have existed for nearly if not as long as the industry itself. The LTCs therefore contain a vast wealth of experience and expertise in establishing, managing and administering all types of wealth management plans and structures, including trusts and PTCs. A Cook Islands LTC will assist the PTC in meeting its statutory and regulatory obligations, as well as other trust activities as the PTC board directs.

Cook Islands LTCs are licensed and supervised in the Cook Islands by the Cook Islands Financial Supervisory Commission.

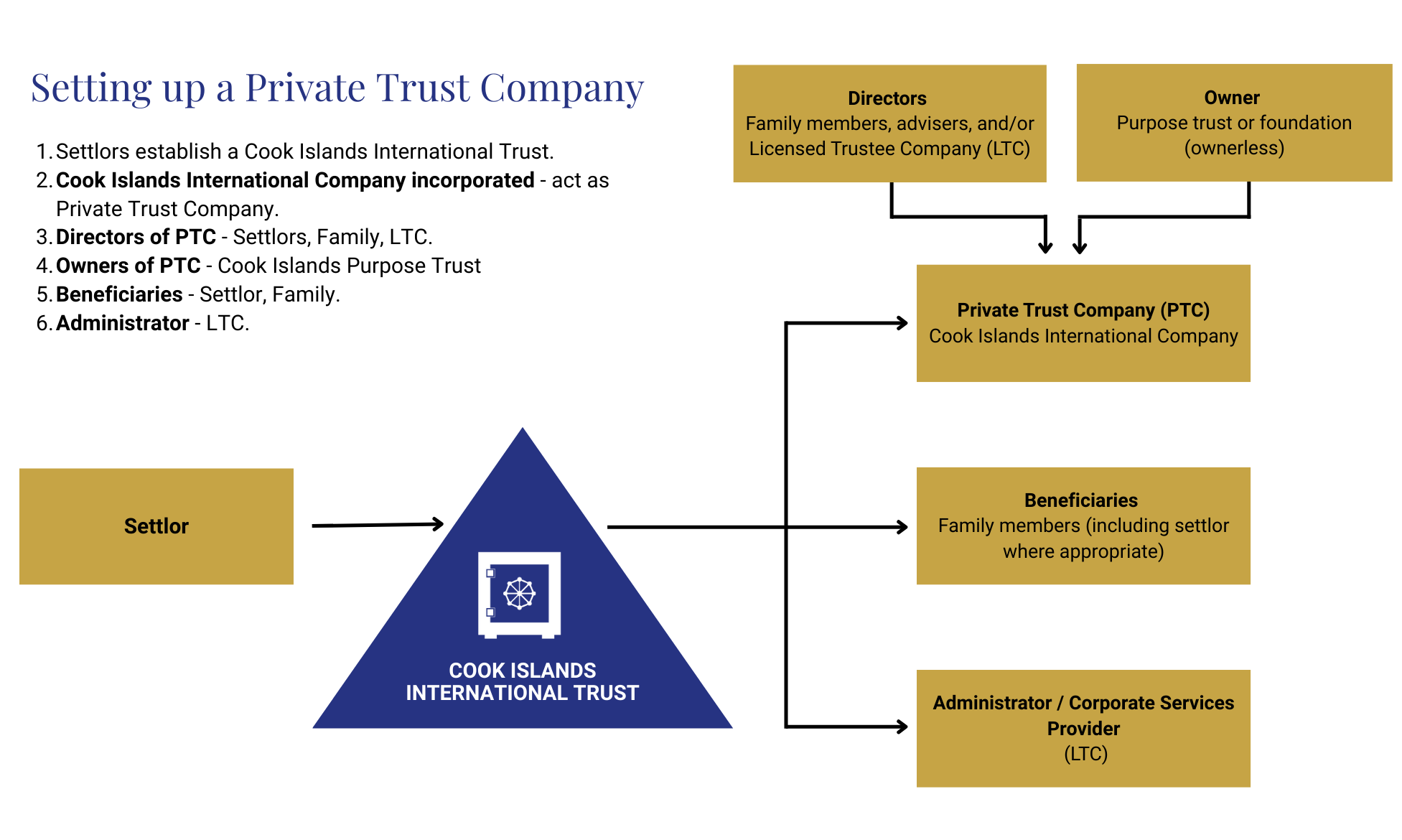

How is the PTC established?

Cook Islands law allows an IC to act as trustee (i.e., a PTC) of no more than three Cook Islands International Trusts (“ITs”) without the IC being licensed to carry on trustee company business. The use of an IC as trustee of an IT meets the Cook Islands legal requirement that one of the IT’s trustees must be an LTC, a registered foreign company or an IC.

ICs must be incorporated through a Cook Islands LTC, with the LTC providing a registered office and company secretary as required by law. The directors of the IC do not need to be resident in the Cook Islands, therefore allowing the settlor to determine the composition of the PTC board. The LTC will incorporate and register the IC to act as a PTC with the Registrar of ICs in the Cook Islands. Details of the settlor(s) and beneficiaries of the IT do not need to be disclosed to the Registrar.

The Board of Directors

The ownership and management of the PTC are vital to its effectiveness and the efficient operation of the overall structure. The settlor’s circumstances and what is best for him/her and their family will ultimately determine ownership and management decisions.

In determining the composition of the PTC board, the settlor must understand that having total control over trust assets may compromise the validity of the structure as well as its tax effectiveness. In addition, it is important to remember that the PTC is a trustee and owes fiduciary and legal duties to the trust’s beneficiaries. The settlor and family members will not (as a professional corporate trustee would) be familiar with the role of the trustee or what is required to discharge those duties. Failure to discharge those duties may lead to personal liability for the directors.

Where the settlor retains too much control over trust assets through the use of the PTC, the structure runs the risk of being considered a sham. Similarly, it may lose tax effectiveness if all substantial decisions are seen to be made in the settlor’s home jurisdiction.

To avoid such scenarios, the directors of a PTC should be a combination of family members and professional advisors, including a professional corporate trustee.

It is most unlikely that the settlor and his/her family members would have experience in administering a trust and its assets. It is therefore advisable that the PTC board engages a professional corporate trustee to provide administration services to the PTC to ensure it meets statutory, regulatory and compliance obligations, and properly documents trust activity, such as investments, distributions, financial transactions and asset transfers.

A Cook Islands LTC can provide a corporate director and administration services to the PTC to enable it to maintain its objectivity, meet statutory obligations and ensure trust activity is properly carried out and recorded.

Ownership Structure

There are a number of options a settlor might consider when deciding on the ownership of the PTC. The most favourable is for the PTC to be ownerless, as this will distance the settlor from ownership, reducing the potential for (i) the structure to be compromised through the settlor not having divested ownership of trust assets sufficiently, and (ii) the trust being taxable in the hands of the settlor.

Two vehicles commonly used to create an ownerless PTC are a purpose trust and a foundation. A purpose trust is a trust established for a particular purpose, as opposed to being for the benefit of named beneficiaries. In the PTC scenario, the trust’s sole purpose would be to hold shares in the PTC. A foundation is created by a founder and managed by a foundation council, similar to a board of directors. Although it is an incorporated entity, the foundation has no shareholders or beneficiaries with proprietary interests. A foundation is established to carry out certain activities or achieve certain objectives. In the PTC scenario, that objective would be to hold shares in the PTC.

Should the settlor wish to hold shares in the PTC directly, he/she should be mindful that in addition to this potentially compromising the overall structure and its tax effectiveness as previously mentioned, in the event of the settlor’s death the PTC shares will form part of their estate and may result in the ownership and control of the PTC, and the succession of the trust assets, being different to what they had intended.

When structuring the ownership of the PTC, the Cook Islands LTC can provide an ownerless vehicle to hold the shares of the PTC through either a purpose trust or a foundation. Cook Islands law provides for non-charitable purpose trusts where the specified purpose will be to hold the shares of the PTC. Similarly, a foundation could be established pursuant to the Foundations Act 2012 for the purpose of holding the shares. The LTC will be able to provide a trustee to the purpose trust and a member to the foundation’s council and administration services to both, if the settlor so wishes.

In the event the settlor wishes to hold the PTC shares directly, despite the potential pitfalls previously mentioned, the Cook Islands can provide a solution to assist the settlor’s succession planning and avoid the PTC shares falling into their estate upon death. Section 228B of the Cook Islands International Companies Act 1981-82 allows the settlor to specify in the PTC’s articles of association, a person or persons to whom they wish the shares to be automatically transferred upon their death and therefore avoiding the probate process.

PTC Protection

A trust must be registered in the Cook Islands as an IT to obtain the benefits of the ITA and its asset protection provisions. Once registered, those benefits will apply from the date of the establishment of or settlement of assets on that trust, not the date of its registration. This includes a trust that is established or settled under the laws of another jurisdiction, but later changes to be governed by the laws of the Cook Islands. Once registered as an IT, the protections contained in the ITA will apply to that trust and its assets from the date of the establishment of or settlement of assets on that trust.

The terms of the trust instrument should be carefully drafted to allow for a trustee (PTC or LTC) to resign, or be appointed or replaced upon the happening of certain events and for the governing law to be changed. This is designed to protect trust assets in the event of aggressive creditor actions.

It should be noted that the protections of the ITA will not apply to a trust where the assets were settled knowing that litigation has commenced against the settlor in regards to those assets. The ITA is specifically designed to protect against future or unforeseen creditor claims, not ongoing or existing ones.

Conclusion

Given its compliance with international standards, its legal framework focusing on protecting and preserving wealth and the experience and expertise gained from providing trustee, management and administration services to a global client base for over 40 years, the Cook Islands is perfectly placed to work with settlors and their advisors to achieve all of their wealth planning needs.

In particular, through a carefully structured and professionally administered Cook Islands PTC, a settlor and his/her family can actively participate in decisions concerning their trust and its assets. The integrity of the structure can be retained, the settlor’s succession and tax planning objectives achieved and legal duties to beneficiaries discharged.

For more information on establishing a Cook Islands Trust contact one of our experienced, local trust companies here or download our Cook Islands trust information factsheet.

About the Author

Alan Taylor is the Legal Technical Advisor for Cook Islands Financial Services Development Authority. He graduated from Auckland University in New Zealand with degrees in law and economics and is admitted to the bar in New Zealand. Alan is a member of STEP, the Institute of Leadership and Management and the New Zealand Institute of Directors.

Alan has worked in the international financial services industry in the Cook Islands, Jersey and Singapore. He has held legal, business development and senior management positions in both public and private organisations.

Licensed Trustee Companies

Our Trust companies bring excellence, experience, expertise and integrity.